We’re introducing a proposed liquidity approach for Tezos DeFi that produces practical utility, higher retention, and manifold benefits to the entire ecosystem (for each layer, runtime, and economic sector). The point of focus is the method and plumbing utilized first, and its liquidity needs second. As will be demonstrated, this is not to chase depth for depth’s sake or for reputational aesthetics. Instead, this is intended to place depth where it converts into access, routing, and real market growth.

Let’s start with the surface goal of this proposal. There are many other beneficial byproducts of this approach, but it’s important to be clear that there is a real problem we are solving. If we do this right, it will enable a solution to a longstanding friction, not just for us but for anyone who has ever deployed or will deploy a token on Tezos.

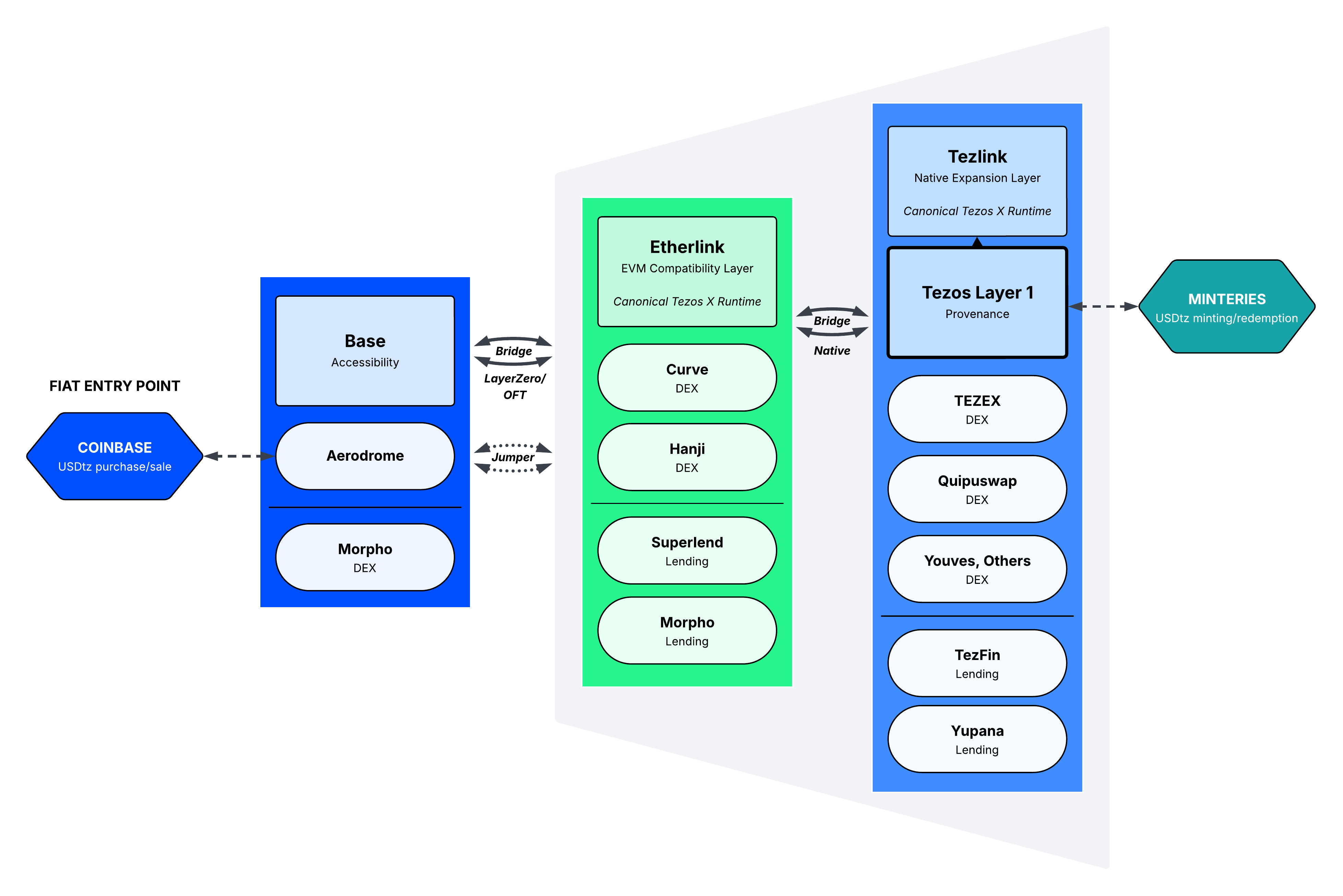

Objective: Make USDtz purchasable through Coinbase’s FIAT on-ramp, whilst doing so in a manner that is decentralized and maximizes ecosystem benefits.

This means achieving a “Coinbase listing” in a manner that is:

-

Decentralized; non-custodial; completely on-chain

-

Circumvents all listing fees (a big financial bottleneck of the past)

-

Tezos L1 provenance-preserving, yet L2 utilizing, as Tezos L1 remains root canonical origin and the asset bridged outward to L2s for utilization (as Arthur Breitman recommended: https://x.com/KMehrabi/status/1955320483240722779)

-

Credit-positive for Tezos, because stable usage recursively expands the surface area for lending and on-chain credit (benefitting lending pools on every layer and runtime)

- Credit which is economically conducive to scaling the Tezos commerce economy (e.g. Art marketplaces)

- Credit which is economically conducive to scaling the staking ratio

-

Market-maker expansionary, because it creates multiple profitable resupply and rebalancing zones (benefitting DEX pools on every layer and runtime)

-

Implicitly demonstrates Tezos X as a whole; enriches Tezos-native (Michelson) runtimes, utilizes the bridges between layers, as well as makes fantastic novel use of Etherlink platforms as an intermediary conduit port-city

-

Designed to encourage a centripetal adoption curve (bringing users from the outside gradually closer to the center of Tezos): as externally-sourced arbitrageur participants naturally optimize their own sourcing and margins, they move upstream toward the Tezos-native origin, pulling activity and liquidity inward into our strategic moat.

In the past, maintaining the benefits of decentralization was contrary to convenient on-ramp accessibility, but that’s no longer the case. Gor years the world wasn’t ready for decentralized methods (and there was a lot of pressure to accommodate centralized vehicles and their centralized methodologies) but now we can have the best of both worlds. In other words, finally those popular centralized vehicles have come to accommodate us and our decentralization-centric ways.

I’ll explain later on why a Tezos-native USD stablecoin is conducive to piloting this program, and why (proudly I say) USDtz is the optimal asset within that framework, but I also want to be clear that this should be the pilot of what virtually every Tezos-origin asset can and should do. Although USDtz provides its own unique benefits to the ecosystems as a staple crop and pure-play asset to showcase Tezos, while also having proven its volume-liquidity strength competitive with any USD stablecoin, in terms of mere distribution and getting listed on Coinbase any asset on Tezos can follow this same path, for which we hope to demonstrate a paved road.

This post:

I. How it works

- Coinbase Listings Aerodrome DEX pool sourcing

- Liquidity Corridor and benefits

- Centripetal adoption dynamics

II. Why USDtz as the pilot

- Why XTZ-USD

- Why USDtz

- Recursive value capture

III. What we still need

- XTZ bridged to Base

- Targeted pool liquidity depth

I. How it works

The idea started when we noticed the exclusive relationship Aerodrome DEX has with Coinbase. Coinbase facilitates fiat on-ramp accessibility for tokens that have liquidity on Aerodrome’s DEX pools. Coinbase started this as a promotion for Aerodrome, sourcing liquidity from Aerodrome pools, but making the assets purchasable with the convenient banking methods that Coinbase has always provided. That alone is great because it enables the best of both worlds: Coinbase’s FIAT on-ramp + Decentralized DEX pools as the source.

The only technical obstacle we had at first for USD Tez (USDtz) was, of course: Aerodrome lives on Base, while USDtz originates on Tezos.

Fortunately, Tezos already gives us the two pieces we need: bridgeability to Etherlink as an EVM-optimized conduit for bridging Tezos-native assets, and the integration of that conduit with LayerZero’s omni-fungible token (OFT) bridge path that reaches Base and Etherlink both. Both bridges are conveniently accessible on the Etherlink website. Moreover, Jumper’s integration with both Base and Etherlink provides a strong method of swapping between blockchains as well.

This to us represents one of the strongest use cases for Etherlink, in which it’s not used as a ‘destination’ but as a conduit for EVM connectivity; a port-city; the ultimate EVM bridge for all of us native Michelson-speaking Tezonians of Tezosland, to reach the greater EVM archipelago.

To enable this, we did a few things:

Others can do this as well for their own assets.

First, we deployed bridge contracts for USD Tez (USDtz) on Etherlink. Meaning, you can now bridge USDtz from L1 to Etherlink, preserving its L1 origin, and benefiting from EVM runtime compatibility. This is conveniently accessed on the Etherlink website.

Second, we deployed the USDtz bridge contract to bridge USDtz from Etherlink to Base. We did this using the LayerZero OFT contract, as its pertaining bridge is also conveniently accessible on the Etherlink website.

Finally, we initiated the initial pools needed to seed liquidity at each layer, on Aerodrome, and Curve (USDC-USDtz), thereby enabling the minimal corridor path (more pools to be added; read on), as well as effectively enabling interchain USDtz swapping on Jumper

Arbitrageurs can probably already imagine how this creates manifold opportunities for them to supply and rebalance the pools, not just between pools or between platforms, but between layers as well.

The asset flow path for arbitrageurs (not the user path, but the asset path; the [retail] user path is the opposite of this) is this:

1. Start on Tezos L1, because Tezos L1 remains canonical provenance (as Arthur recommended, see this video from TezDev 2025)

- Root Arbitrage; mintery-based minting/redemption

(has already been occurring organically for 5+ years) - Interpool Arbitrage/rebalance/supplying for USDtz pools within L1

(has already been occurring organically for 5+ years)

2. Bridge the asset from Tezos L1 to Etherlink to make it canonically EVM optimised

- Interlayer Arbitrage; bridging assets from L1 to Etherlink

- Interpool Arbitrage/rebalance/supplying for USDtz pools within Etherlink

3. Bridge the asset from Etherlink to Base

- Interchain Arbitrage; bridging assets from Etherlink to Base

- Interpool Arbitrage/rebalance/supplying for USDtz pools within Base

This path gives USDtz distribution reach beyond Tezos whilst extending from (and implicitly growing) Tezos’ origin layer, and everything in between (e.g. Etherlink)!

This isn’t just a path; each ‘zone’ of this corridor creates exponentially more economic opportunities whilst distributing manifold anchors of stability.

Multiple profit zones of the liquidity corridor:

This corridor does not create one big market-making job. It creates multiple profit zones. Once USDtz pools exist across Tezos L1/Tezlink, Etherlink, and Base with enough depth, each environment naturally develops its own local economic market respectively. That is, its own rebalancing patterns, its own DEX pools, its own participants, its own lending pools, and its own local pricing beacons.

Inside each environment, participants earn by resolving local imbalances. They arbitrage across pools, rebalance inventory, and resupply where demand drains liquidity. No one has ever coordinated this nor needed to do so. It happens already on Tezos L1 today and has for years, with mini-desks of individuals who noticed the opportunity and applied themselves to earn from arbitrage rebalancing of the various DEX pools, some of whom even work further upstream by minting/redeeming USDtz at the source. The corridor multiplies the number of places where the same organic behavior can occur.

Likewise, some participants may stay inside one environment and arbitrage between pools there (say, on Base alone). Others earn by bridging inventory from one environment into the next when a pool needs supply (i.e. bridging USDtz from Etherlink.) Others will chain multiple hops because tighter sourcing improves margins. Every additional hop adds another surface with its own DEX pools and lending pools where demand can pull against supply, and that creates a more textured network of ways to earn while keeping the corridor healthy.

Each zone makes money by doing one of two things:

- Rebalancing liquidity inside its local venue when flows push price out of line

- Resupplying inventory from an upstream venue when local demand drains the pool

That matters because the corridor naturally splits into stages.

Startpoint:

Coinbase FIAT on-ramp. The first place to get USDtz to rebalance the XTZ-USDtz pool (Aerodrome) would be from the normal and convenient Coinbase listing for USDtz. This is where the user would be able to buy USDtz the way most people buy any asset.

The USDtz supply that Coinbase sources would come from the USDC-USDtz stableswap pool (Aerodrome), which would enable purchasing at high depths without slippage. The more pressure that builds on that pool, the more it would need to be rebalanced. This informs the first “wholesale” level arbitrageur activity.

Base (downstream):

These arbitrageurs focus on the Aerodrome USDC-USDtz pool and other USDtz pools on Base. When Base demand pulls USDtz out of balance, they arbitrage and rebalance locally. But when Base keeps pulling, local rebalancing is not enough, they need inventory. So, naturally they’ll start bridging USDtz from its closest hop upstream (Etherlink), because upstream has the raw wholesale supply.

- Bridge:

- Jumper (USDtz-other assets) - LIVE

- Etherlink-EVM Bridge (OFT/LayerZero; USDtz-USDtz) - LIVE

- DEX:

- Aerodrome (USDC-USDtz) - LIVE

- Aerodrome (XTZ-USDtz) - requires XTZ bridge contract deployment

- Lending:

- Morpho (not an immediate necessity but eventually with depth)

Etherlink (midstream):

These participants sit one step upstream and specialize in the Etherlink venue(s). They rebalance Etherlink liquidity, but more importantly, they act as a resupply depot for Base. This is how Etherlink serves as what can make it most valuable, as I’ve always called it: an EVM port city for Tezos. When Base desks need inventory, Etherlink becomes the nearest wholesale source. So these participants can pull from Curve or potentially Hanji, or from Superlend. Etherlink desks profit by bridging inventory to Base when spreads justify it, and by keeping Etherlink pools balanced so that inventory stays available.

- Bridge:

- Jumper (USDtz-other assets) - LIVE

- Etherlink-EVM Bridge (OFT/LayerZero; USDtz-USDtz) - LIVE

- DEX:

- Curve (primary for re-suppliers; USDC-USDtz) - LIVE

- Hanji (companion for CLOB trading; XTZ-USDtz)

- Lending:

- Morpho (not an immediate necessity but eventually with depth)

- Superlend (our preference; as closer to ‘Tezos-centric’ strategy)

Tezos L1 (upstream, ‘root-adjacent’):

These participants operate closest to the canonical origin. They source USDtz at the root and supply it into the corridor. They profit when downstream demand pulls inventory outward, because they sit at the best wholesale entry point. Again, it’s better to start Tezos assets from L1 and bridge them over to L2s, rather than mint on L2s directly. This increases ability to interoperably bridge to different L2s, as well naturally increase retention, as adding a layer of abstraction reduces propensity for withdrawals.

- Bridge

- Tezos L1-Etherlink Bridge (USDtz-USDtz) - LIVE

- DEX

- 3route (Aggregation) - LIVE

- TEZEX/Quipuswap/Others (XTZ-USDtz, USDtz-USDT) - LIVE

- Lending

- TezFin (USDtz) - LIVE

Minteries; Minting/redemption (root):

Farthest upstream still are those that actually go through the process of minting and redeeming USDtz, which we call ‘minteries’, some of which operate as services. Minteries are Tezos bakers who are also enrolled with USDtz as minters. Everything downstream of this step emerges organically and self-propagates, just as it always has. Some platforms (e.g. Objkt) and FIAT on-ramp institutions (e.g. Wert) have and can enroll as direct minters.

Natural Centripetal Adoption

A participant can start downstream on Base, earning by rebalancing the Aerodrome pool. To keep doing that, they need inventory. They source from the nearest upstream environment, which is Etherlink. That is, they’d buy from Etherlink, bridge it over to Aerodrome where supply would be scarcer, and earn from the differential.

If they keep sourcing from Etherlink every time, they’ll earn but some people will eventually realize that they keep paying the upstream spread. The more profit-driven operators then move upstream so they can source cheaper and more reliably. Over time, some move further upstream still, because the best wholesale sourcing sits closest to the root origin on Tezos L1. That is, to get the fuller value, they’ll go to the source.

This upstream migration is not required for the corridor to function. But it is a valuable emergent effect: Base-side demand brings in new participants, and some of those participants naturally climb toward Tezos provenance as they optimize.

To get someone on Base to inch their way upstream until they get a Tezos wallet with a Tezos account and tz-wallet address is a home run for the ecosystem!

II. Why USDtz as the pilot

There are 2 questions to answer here:

- Why USDtz? (literally as in why is it so special for the ecosystem)?

- Why USDtz as the pilot for this particular program?

The answers might sound counter to expectations but that’s also why they need to be explicated. I’ll stick to what’s practical and deliberately avoid ideological reasoning as those tend to ‘not matter’ to most audiences when talking stablecoins, and also because they aren’t necessary (and perhaps distracting) in making this larger point:

-

Volume! Strong and Organic: USDtz arguably outperforms other reserve-backed USD stablecoins As a USD stablecoin, it naturally generates high-frequency usage and sustained contract interaction and this has been demonstrated over years. This has been evident as USDtz has generated hundreds of millions of dollars in volume (that’s genuine contract-trading volume, not mere transfer volume) with a micro-amount of liquidity. Most reserve-backed USD stablecoins on DEXs get roughly the same volume-to-liquidity activity. If there’s a price to rebalance and money to be made, users act on it as they always have for the past 5-6 years of USDtz.

-

Distributed Participation: USDtz moves in many micro-pocket interactions (not just one or two whales with an arb-bot hooked up to a Binance), and this has always cast a relatively wider participant net for USDtz. This fact might sound counter-intuitive but this is also a big reason why USDtz has more holders than Tether on Tezos and has had a better volume-to-liquidity ratio. It achieved this atomicity not despite its lack of being on so many CEXes/access points but actually and ironically because of it. Large whales and institutional traders naturally absorb all the market opportunity away from retail participants.

-

Tezos pure-play proof-of-concept: USDtz is single-chain origin; it exists as a stablecoin for Tezos, not as an accessory to a multi-chain asset, so we can more discernibly measure its interactions as conscious deliberate plays, and its successes as Tezos successes. USDtz is a defendable market and showcase of XTZ capital market potential that cannot be diminished as having achieved volume or activity as spillover from other chains’ success or as exit liquidity. If you’re using USDtz it’s because you’re intentionally using Tezos, period.

-

Strategic optionality: Proving this corridor makes it easier for other major assets to justify coming to Tezos natively (including and especially USDC), and it makes it harder for existing major assets to treat Tezos as expendable when activity is thin (USDt has dropped 5 chains in the last 2.5 years). No one can ever take USDtz away from the ecosystem or threaten to leave without getting more money. USDtz has nowhere else to go, and that’s a good thing!

-

Balance-sheet stickiness (reduced flight risk): USDtz creates retention dynamics that USDC cannot. USDC is designed to be universally fungible and therefore functions as an instant escape hatch in volatile moments, which increases the probability of liquidity cliffs. USDtz, by contrast, is most useful inside Tezos-native flows and therefore naturally encourages internal rebalance and reuse instead of reflexive exit. That makes XTZ-USDtz liquidity meaningfully more resilient and less prone to disappearing the moment sentiment turns.

-

Endogenous price discovery (sovereign signal): XTZ-USDtz produces price discovery that is native to the Tezos economic graph, rather than merely reflecting price discovered elsewhere and imported through arbitrage. That distinction matters because the ecosystem needs internal market signals it can trust when building credit, risk models, liquidation logic, and commerce pricing. XTZ-USDC trading can be useful, but it anchors the quote leg to an external monetary primitive and makes Tezos markets downstream of other venues. XTZ-USDtz strengthens Tezos as a self-contained market rather than a mirror.

-

Credit-layer alignment (cleaner liquidation and collateral paths): USDtz is structurally a better quote currency and settlement asset for Tezos-native lending than USDC because it aligns the stable leg, collateral flows, and liquidation pathways inside the same economic domain. When the main stable leg is external, the system inherits extra issuer and venue dependency, and liquidation routing becomes more fragile under stress. A deep XTZ-USDtz market is not just a trading pool, it is base infrastructure for a robust lending and debt economy on Tezos.

-

Composability density (more work per dollar of liquidity): USDtz increases composability density per unit of liquidity because it can be reused across Tezos-native trading, lending, payments, RWAs, and future derivative rails without breaking identity or requiring users to switch monetary domains. USDC can touch many venues, but that breadth often fragments capital across chains and incentives. USDtz concentrates reuse into a single coherent economic graph, which increases velocity and capital efficiency. In practice, fewer dollars of USDtz liquidity can do more ecosystem work than the same amount paired with USDC.

-

Asymmetric downside protection: USDT can leave Tezos (NOTE: they already left 5 chains in the last few years) or start asking for exorbitant monetary compensation to stay. If it leaves, liquidity and market structure vanish instantly. USDtz has nowhere else to go (outside of being redeemed at a root level), which is exactly why it is a stronger base-layer stable for Tezos. That creates an asymmetric strategic advantage: the downside of relying on USDtz is bounded to the health of the Tezos ecosystem itself, while the downside of relying on USDC includes the risk of external strategic abandonment. An XTZ-USDtz pool therefore strengthens the ecosystem’s long-term continuity in a way an XTZ-USDC pool never can.

BYPRODUCT OF DEPTH: Establishing depth for USDtz also enables its own financial self-sufficiency (via GENIUS Act mechanisms)

USDtz depth also enables self-sufficiency through the specific GENIUS Act return mechanisms. Depth turns that structure into real financial output that can be directed back into ecosystem operations and reward pathways, instead of relying on one-off support.

This is also why it makes for a better pilot than even ETHtz or BTCtz (some have asked why aren’t we pushing for the other two StableTez assets, ETHtz and BTCtz, at the moment).

These returns will not only cover costs, but enable real reward flows concentrated to users in the Tezos ecosystem (not split across multiple chains), and finance fund reserved for the future StableTez DAO. The StableTez DAO will not only manage its on-chain treasury fund but work towards further evolving administrative components that are off-chain to on-chain administrative frameworks.

III: What we still need

We’ve deployed the contracts and created the pools for most things but a few outstanding last mile needs to complete the circuit.

There are multiple ways to seed and deepen USDtz liquidity, and they are not mutually exclusive. The right approach depends on what you are optimizing for first: immediate depth, retention of liquidity, or long-term self-sufficiency.

1. Bridged XTZ from Etherlink to Base

Although we have bridged USDtz to Base using the bridges accessed on the Etherlink website and have established a USDC-USDtz pool, we also need an XTZ/USDtz pool on Aerodrome.

But, believe it or not, XTZ is still not bridged to Base. Technically we can deploy the bridge ourselves by deploying the same bridging contracts, but that wouldn’t be ‘canonical’ when it comes to explorers identifying it as verified.

To do this correctly, we need a canonical, registered, verified Tezos-origin representation of XTZ on Base. Bridging capacity exists, with LayerZero’s Etherlink integration for OFTs but the market needs canonicity and verification. Without that, LPs, routers, and most importantly, explorers do not list the asset as the real thing. (In other words, someone with an @tezos.com email address needs to verify it for BaseScan to list it, and therefore for Aerodrome and others to represent it without a warning notice)

2. Liquidity Depth for the pools

Liquidity depth is the practical requirement that turns this corridor into a usable on-ramp path. With depth, routing becomes reliable, execution stays tight across trade sizes, and professional participants can keep spreads compressed through routine resupply and rebalancing. Depth for this liquidity corridor structure makes the system self-reinforcing: once execution is consistent, volume concentrates, arbitrage becomes continuous, and the corridor starts to maintain itself through normal market behavior rather than episodic support.

USDtz makes this a uniquely strong opportunity to build that kind of recursive liquidity because it is a USD stablecoin and it naturally generates high-frequency flow. Add the XTZ pairing leg and you create a persistent instrument for both stable routing and Tezos exposure. That combination supports recurring demand, recurring volume, and recurring arbitrage, which is what lets liquidity deepen and compound over time.

The ecosystem has, of course, used specific methods to bootstrap depth in the past (e.g. Apple Farm), and those have ostensibly ended.

That creates room to learn from those experiments, try different approaches, run tighter experiments, and iterate toward liquidity structures that are durable rather than dependent. This specific corridor strategy and its associated pools presents not only an ideal pilot for true utilization but is one in which retention and recursive economic benefits are implicit in the design.

Which pools need depth

On BASE

Aerodrome: USDC-USDtz pool (live)

Aerodrome: XTZ-USDtz pool (once XTZ is bridged to Base by the appropriate party)

Through these two pools,

-

Day Trading Pool (high constant volume): Users come in from Coinbase and conduct XTZ-USD trading and spot arbitrage as they have for years. XTZ-USD tradeability and with a pool (XTZ-USDtz) under-tapped by institutional arbitrage bots (unlike XTZ-USDC or XTZ-USDT). They’d be able to buy XTZ and USDtz through Coinbase.

-

Supply Pool (resupplies Coinbase): The primary purpose of this is to make USDtz purchasable on Coinbase. The more people buy USDtz on Coinbase, the more pull on the USDC-USDtz pool, which itself would need resupply for USDtz. This leads arbitrageurs to go to the nearest neighbor source (Etherlink).

[Bonus BD Opportunity: If depth is enabled via some form of an incentive program, it opens the door to one of the ways the ecosystem can have more direct cooperation with Aerodrome/Base/Coinbase in a lovely way. E.g. joint-promotions in which Aerodrome can in part reward users with AERO tokens, and in part the ecosystem provides its own rewards. That dual-channel reward structure is also a great ‘lure’ for outsiders coming from an Aerodrome/Base, to try out Tezos, making them more likely to take a hop-step closer towards Tezos-proper. Just saying..]

How to reward Base liquidity adding activities: LP tokens can simply be bridged from Base to Etherlink, or LPs can be rewarded on Base itself. Either way, the Tezos stack is demonstrably implicit by way of the stack.

On ETHERLINK

Depth for the supply pools on Etherlink. Arbitrageurs will then venture to Etherlink to get their resupply inventory for the Aerodrome USDC-USDtz pool. Etherlink is the nearest supply depot or port-city for which to acquire and export USDtz to Base via bridging. Of course, It’s EVM and interoperable with tools and platforms these Aerodrome/Base arbitrageurs already use. Moreover, the USDtz tokens are already EVM optimized as they were bridged to Etherlink using the canonical bridge contract.

Pools:

Curve: USDC-USDtz pool (live)

Hanji: XTZ-USDtz (requires pool deployment)

Superlend: USDtz (requires pool deployment)

On Etherlink, Curve can serve as the major supply clearinghouse for USDtz swapped with other stablecoins, while Hanji (being a CLOB) can serve as an additional price-setter specific, to Etherlink runtime.

On TEZOS-native (Michelson runtimes)

Of course this is the origin point from which trust is established. Arbitrageurs who ventured from Base to Etherlink to edge their margins will realize that they are simply buying the liquidity in pieces that others bridged from the Tezos L1 to Etherlink. In this way we bring them over to the root of Tezos, the L1. At which point (gaining comfort in this area by way of exposure) toward where the Tezos ecosystem’s strategic moat resides. This would necessitate liquidity depth for basic Tezos DEX and Lending pools.

DEX Pools:

TEZEX: XTZ-USDtz (live) (Tezlink upgradable)

TEZEX: USDt-USDtz (pending) (Tezlink upgradable)

Lending:

TezFin: USDtz (live) (Tezlink upgradable)

Yupana: USDtz (requires pool deployment)

Note on How to reward Tezos L1 liquidity-adding activities without L1 middleware: We do not need L1 middleware to reward users for adding liquidity to L1 pools. LP tokens can simply be bridged from the Tezos L1 to Etherlink. That circumvents the entire ‘lacking middleware’ bottleneck, without having to develop it on the L1. In fact, we already began doing this with LP tokens from Tezos L1. That is, you can now go to the Tezos L1-Etherlink bridge and bridge your ꜰTokens (ꜰUSDtz, ꜰUSDt) from Tezos L1 to Etherlink. All rewards programs (farming and such) can be done there. No L1 middleware needed; Presence of those bridged LP tokens on Etherlink is clear implicit evidence that the user completed the L1 liquidity-adding activity.

Other assets

We’d like to continue this path with other assets. USDtz-xU308 and USDtz-stXTZ are two pairings in particular that would have immediate utility for routing, price discovery, and credit formation across the Tezos stack. USDtz-xU308 enables direct price discovery and liquidity between a Tezos-native USD stablecoin and a Tezos-origin real-world asset, anchoring an RWA to a Tezos-native fiat reference while supporting credit formation around commodity-backed collateral. USDtz-stXTZ does the same for a liquid staking token, keeping routing and credit paths inside the Tezos economic graph while making staked Tez exposure accessible across DeFi without giving up its liquid state.

From Attraction to Compounding

In summary, beyond a decentralized solution to a long-standing utility problem, this proposal serves as a pilot blueprint for an export-driven liquidity architecture: it imports externally sourced participants and liquidity, turns that flow into on-chain opportunity across multiple venues, and compounds it directly into Tezos-native markets. The corridor is as decentralized as it is rewarding, because it creates many independent ways to participate and earn while strengthening the Tezos stack across Layer 1, Etherlink, Tezlink, and the sectors beneath them. The result is a system that enfranchises multiple layers and sectors of the Tezos economy through real usage and on-chain incentives.

At a deeper level, this approach is about the difference between merely attracting temporarily liquidity and actually compounding it. Incentive programs that target the lowest-friction edge of the periphery, without any export path or centripetal pull toward underlying layers, can attract activity but struggle to retain or multiply it. By contrast, a corridor that begins with Tezos-sovereign assets and gives participants a clear, margin-driven reason to move inward creates a structural path from attraction to retention to recursive compounding. This is what allows capital to circulate rather than churn. It also sets the conditions for finance to meaningfully integrate with the real economy already present on Tezos, where commerce provides durable participation and finance provides efficient capital formation. Bringing these pieces together through an export-driven, credit-positive liquidity architecture is what turns usage into reinforcement, and reinforcement into a self-sustaining system; a true virtuous cycle.