The tax burden for staking rewards when they are claimed as income is pretty high. I think you could have a token that collects the baking rewards in its own pool and is backed by more and more XTZ as it gets rewards. Then the token holder could hold for a year or more to take advantage of long term capital gains. It also has the potential to eliminate a lot of the discrepancy between tax jurisdictions (your stake doesn’t get diluted relative to others just for living in a certain place). I think it should be simple enough to make and would provide immediate utility.

The token contract itself earns the rewards. The XTZ pool that the token is backed by will increase relative to the token amount. Then you could choose to sell the token or withdraw your share of XTZ from the pool.

I am not capable of making this myself but wanted to share the idea for those that might be.

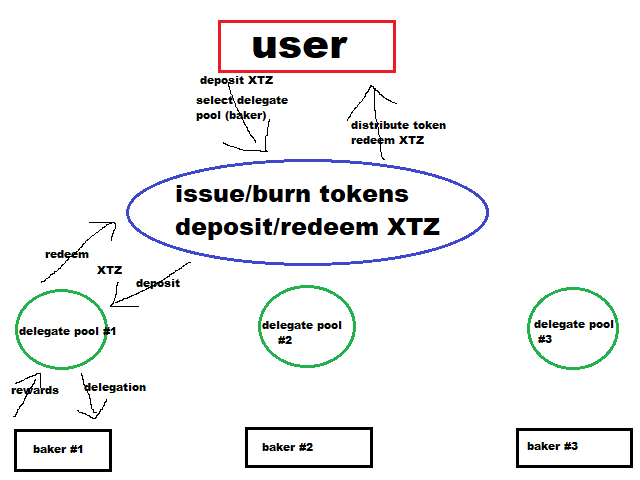

Just a quick and dirty pic of how I think it could work

Disclaimer - I’m not a tax lawyer or CPA, so this opinion is not authorative, do your own research. But my understanding is that in the US, when your receive a staking reward, that is not a capital gain itself, it is treated as ordinary income. You would calculate that income as the number of XTZ you received times the price in USD at the time you receive it. You would have to pay tax on the ordinary income in that tax year.

That price also becomes your basis price. If you later sell at a price above the basis, the difference becomes your capital gain.

What I’m saying is, you’d still be liable for the ordinary income for the year you received the staking reward, even if your XTZ was in a contract. You would pay short-term or long-term gains tax separately, depending on when you sold.

Again, this is just my opinion, do your own research to confirm.

It is a little ambiguous whether exchanging your tokens with the contract will result in an ordinary income event. It is my intuition that if the tokens were exchanged with the contract for XTZ it would be an exchange and not a distribution, and not necessarily an income event. Consider the case where someone buys the tokens from someone and then exchanges them for XTZ. It doesn’t make sense that it would be an income event for them.

However, even if it were considered a distribution, you could take advantage of long term gains by selling the token directly. I want to point out that this is not specifically about changing gains from short to long term, but allowing for stakers to choose the time that the taxable event occurs. Although LTCG will be a motivation for many people, simply being able to choose the timing of the event is extremely powerful by itself.

Taxation of POS rewards is burdensome - as it is based on outdated taxation principles poorly aligned with the reality of POS networks.

In the US and many other jurisdictions, the current guidance appears to be that rewards are taxable as income based on their fair market value on receipt. The (taxable) fair market value upon receipt then becomes the cost base on which future dispositions may give rise to capital gains or losses (subject to the specific costing rules applicable in your jurisdiction).

Groups such as the POS Alliance are pushing the US Congress to limit taxation to gains on disposition. Still, even if the IRS adopts this position, it might only apply to bakers that receive rewards directly from the protocol. There is a good chance delegators who receive their rewards from bakers wouldn’t benefit from the desired policy change unless delegator rewards flow directly from the protocol itself and bypass bakers altogether.

While the specific rules vary by jurisdiction, in the US at least, the IRS takes the position that a taxable disposition occurs when one virtual currency is exchanged for another - so any token/XTZ swap scheme would likely increase rather than lower the compliance burden and potential for taxable gains or losses (see, for example, https://www.irs.gov/publications/p544#d0e7171).

Special DAOs and pooling schemes may prove useful from a tax perspective if you can avoid creating multiple taxable transactions as you move in and out of them, but as soon as someone - or something - holds another person’s assets to generate profits/returns, securities compliance, KYC and other related issues almost always follow.

Disclaimer: This information is provided for reference only and should not be relied upon. Always obtain your own qualified professional legal and taxation advice.

I think you are correct that it would almost certainly be the case that any PoS rules adopted by congress re:disposition in the US will only apply to direct bakers and not delegation. That is one of the reasons a token like this will have continued utility.

The question you are hinting at in this situation is whether the IRS (or other authorities) will have jurisdiction over the contract/DAO earning the rewards. It will be important to establish a clear path to a non-taxable jurisdiction during deployment and maintenance.

I do not think would be accurate to describe this DAO as “holding another person’s assets.” But it will definitely be important to make that clear legally and practically as part of deployment. Or alternatively, someone could just make it and release anonymously - leaving all those questions up to the individual who decides to use it